But in hindsight, Bazalgette’s beautiful sewer, which was imitated across England, contained a fatal flaw: household sewage and stormwater drainage ran through the same set of pipes. Even today, heavy rainfall can cause the system to overflow, sending untreated waste straight into rivers.

Reputation down the toilet

It’s the job of England and Wales’s 17 water companies, privatised by Margaret Thatcher in the 1980s, to try to stop this from happening. Their increasing failure to do so – or the public’s increasingly low tolerance for any such failure – has created a new Great Stink for the 21st century.

And lodged in the heart of this fracas, at least as the public sees it, is an Australian company: the omnipresent Macquarie Group.

Its 2006-17 part-ownership of Thames Water is widely perceived as the catalyst, or epitome, of everything that has gone wrong: the struggling sewers and filthy waterways, the high household water bills, and the sector’s sometimes parlous corporate finances.

“It has really hurt Macquarie in terms of its reputation in the UK, no doubt about that,” says one seasoned local infrastructure investor.

He doesn’t hold Macquarie responsible, but many do. The unravelling of Thames Water – which is now teetering on the verge of debt default and special measures – is frequently sheeted home to the Macquarie period, when Thames Water supposedly dosed up on debt and juiced up its dividends.

In the wash-up, the unforgiving British press labelled the Australian financier a “vampire kangaroo”. Macquarie has since largely trod the safer terrain of digital infrastructure and renewables investments, but it has never quite shaken the moniker from its back.

Aussie exposure

More recently, Macquarie has donned a kind of hair shirt: it has pumped more than £1.6 billion ($3.1 billion) of equity into arguably the second-most fragile of the English sector’s regional monopolies, Southern Water, with a clear intent to do things differently.

“Macquarie has been so burnt by the perception of what happened at Thames Water that it wants to demonstrate that it knows how to run a water company,” says one industry observer.

But Macquarie’s fresh investment means that its exposure to the fallout from the Thames Water crisis is not just reputational. It’s also material: if, or when, the crisis boils over at Thames Water, it could easily spill into the sector at large.

And that also applies to the clutch of other Australian investors in English water assets, including QIC, IFM Investors, Igneo, REST, Spirit Super, Prime Super and SAS Trustee Corp. If Thames Water goes down, so, too, potentially, will the value of investments that ultimately belong to Australian workers and pensioners.

One of Joseph Bazalgette’s London pumping stations, still partly in use to this day. Bloomberg

The reckoning is coming soon. On July 11, regulator Ofwat will set out its requirements for every English and Welsh water company for the five years from 2025.

In an initial ruling, which may only be the first salvo in a year-long battle, the companies will learn how much investment Ofwat wants them to sink into their networks, how much they can jack up bills to pay for it, and how much they can send to shareholders.

For the industry and its investors, it’s an anxious wait. They’re worried that Ofwat’s priority is to please its political masters, whose antennae are tuned firmly into the public outrage on both waterway pollution and the cost of living.

This means Ofwat could hit the companies from both sides, capping bill increases while also demanding more investment into sewerage works.

Ofwat chairman Iain Coucher recently signalled as much. In a letter to the companies in March, he said the number of serious pollution incidents was “still too high” and “the pace of reduction not fast enough”. But “some companies are still paying significant dividends while failing to meet their environmental targets”.

Just in the past few weeks, South-West Water has come under fire from a cabinet minister, who expressed “anger and frustration” at the company for having the temerity to pay a dividend while fighting a major cryptosporidium outbreak.

If the regulator takes a tough line, Thames Water may have to go into special measures – and the effect of that could cascade throughout the sector. A shift in perceived risk, particularly regulatory risk, could rattle creditors. And it could sap the value of the equity stakes held by Macquarie and the Australian superannuation funds for years to come.

“The way Ofwat is behaving has alarmed a lot of investors and has caused them to reweight the risk of the whole sector,” says one industry player.

A year of potential turmoil lies in store. But just how much of it really lies at the feet of Macquarie? And if it wasn’t the vampire kangaroo, who has been the real villain?

Macquarie’s time at Thames

The case for the prosecution has been made repeatedly in the media. Macquarie saw a company that was generating a solid, regulated annual return, but was not exploiting it. Through securitising the entire business, via a holding company, it could ratchet up Thames Water’s gearing.

A clutch of Macquarie’s funds joined with other investors, some of whom have stuck with Thames Water, to buy the company from RWE for £2.3 billion in October 2006. Macquarie’s contribution was £1.1 billion, for a 48 per cent stake.

Thames Water is trying to dig itself out of a debt hole. Bloomberg

Macquarie and its co-investors then set about increasing the ratio of debt to regulatory capital, hitting 80 to 90 per cent in an industry where gearing is normally about 60 per cent. This funded an initial dividend payout in 2007, cementing the idea that Macquarie was loading up the company with debt to fund shareholder returns.

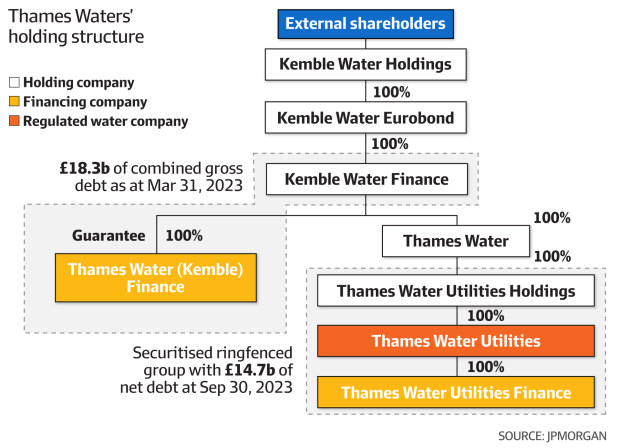

The general view among industry figures contacted by The Australian Financial Review was that all the companies were ramping up debt over this period, but Thames Water was a notable enthusiast. Its particular trick was to add a significant tranche of junior debt at the level of the parent company, Kemble, outside the regulatory ringfence that constrains borrowing at the operating company.

“Most people would feel that the behaviour of Macquarie was exceptional compared to the others. The gearing was higher than all the others. Then, when things became challenging, Thames Water had fewer resources on which to draw,” says one insider.

In this telling, a roughly £17 billion debt pile left Thames Water ill-equipped for the past few years, when borrowing costs and input costs have risen, and when Ofwat has been busily stepping up penalties and keeping bill revenues in check.

“If the original shareholders profited at someone else’s expense, it was first and foremost at the expense of the investors who subsequently bought over the original shareholders’ shares at big premia in the decade or so that followed,” John Earwaker, director of First Economics, said in a recent note.

“Most of these shareholders are now paying a heavy price for buying a company with a capital structure that, in actual fact, is not as efficient as it was sold to them.”

Macquarie, unsurprisingly, sees things differently. At its annual meeting in July, chairman Glenn Stevens and chief executive Shemara Wikramanayake railed against the British media for taking what Wikramanayake called “a very narrow narrative on things”.

The company followed up in August by publishing a “factsheet” to set out its detailed case. Macquarie argues, in effect, that looking at absolute metrics like debt and dividends ignores what really went on at Thames Water during the fund manager’s 11-year tenure.

Although debt jumped from £6 billion to £11 billion over the period, the regulated asset base – the investments Thames Water made in infrastructure that can be recouped from future bill revenue, generating returns for investors – expanded from £6.5 billion to £13 billion. On that measure, the gearing ratio declined.

It also says its own favoured measure, the debt-to-EBITDA ratio, largely stayed at 6 to 7 times, much like most other utilities, until the regulator put the squeeze on permitted returns in the mid-2010s.

On distributions, Macquarie says these totalled £1.1 billion over 11 years, comprising £879 million of dividends and £277 million of interest on shareholder loans. Of this, Macquarie’s funds – or, more precisely, the institutional investors in those funds – absorbed £508 million.

Another tranche of distributions, totalling £1.6 billion, were not dividends but what Macquarie called “inter-company movements” – money shifted from the regulated operator Thames Water to the parent Kemble to repay the junior high-yield debt.

This meant the average annual yield on equity to the 2006 investors was 5 per cent, plus 7 per cent capital growth, for a total of 12 per cent a year. Britain’s publicly listed utilities averaged a 10 per cent total shareholder return over the same period, Macquarie said, so Thames was not exceptional.

The factsheet makes unusual reading because, in the interests of reputation management, it almost seeks to downplay the relative success of the investment – not a trait normally associated with Macquarie.

But Macquarie does try to contrast its own stewardship with that of the subsequent owners, fielding data that suggests Thames Water’s capital expenditure, regulated capital value and some of its debt ratios have worsened since 2018.

For good measure, it also suggests that Thames Water’s investment in infrastructure – as measured by inflation-adjusted average annual capital expenditure – was higher under Macquarie ownership than when the utility was government-owned in the 1980s, when it was publicly listed in the 1990s, and when it was owned by RWE in the early 2000s.

On the nose

But try telling all this to the public. The water companies have, in the past four to five years, become among the most toxic organisations in the country.

Their suspicion is fuelled by a media storm. The Times has run a year-long campaign against the water companies. Private Eye has a special section called “Turd of the Week”, singling out the chief executives’ remuneration, or lambasting the distribution policies. The 1980s pop singer Feargal Sharkey has been reborn as an activist.

Sewage mixes with stormwater at an overspill in a village in the Thames Valley west of London. Bloomberg

Labour under Jeremy Corbyn promised to renationalise the entire sector – one of the few Corbynite pledges the electorate actually warmed to. The Liberal Democrats are hoping to rev it up as an election campaign issue. The New Statesman recently cited a poll of 6000 people who voted Conservative in 2019, in which more than half said they would consider the government’s handling of the sewage crisis when voting this year.

“It has really taken off in the last two years. It’s amazing how quickly this has shot up in the public consciousness,” says Peter Hope, an economist at Oxera Consulting.

One reason, says David Henderson, CEO of the industry body Water UK, is that since 2021 Britain has had one of the toughest regimes for policing overspills and pollution.

“The government brought in legislation to monitor all the overflows. Nobody else does that. France doesn’t know how many overflows it has, but in the UK we know what the problem is,” he says.

But at the same time, government budgetary belt-tightening has eroded the Environment Agency’s capacity to police the network and companies, and to maintain the public’s trust that the government is on top of the problem.

When you then add in the difficulties that the debt-heavy companies have encountered as interest rates and energy costs spiralled, things look grim.

But appearances can be somewhat deceptive. Moody’s Investor Service this year took on the job of figuring out whether the problem is actually any worse in England than elsewhere. And its findings would surprise the singularly disgruntled Brits.

“Treatment of wastewater is good, with more extensive sewage networks and more intensive treatment than other developed economies,” Moody’s analysts reported.

“Although the widespread use of combined sewers results in discharges to waterways, we can find no evidence that this is greater than in other countries, where overflow events are subject to less monitoring.”

England compares favourably with Australia on many metrics, including sewage treatment, although the English system is much leakier. Incredibly, England’s coastal sites score better on World Health Organisation-equivalent guidelines than New South Wales.

Another telling statistic in the Moody’s report is that the water utilities in Scotland and Northern Ireland, which are state-owned, perform less well than privatised England and Wales on almost every measure. So much for nationalisation as a solution.

The one area where England is a clear laggard is customer satisfaction. “British households report lower confidence than those in other wealthy countries that water companies are ‘doing enough’,” Moody’s says.

“This perception creates social risks for water companies because it makes it harder to convince consumers to accept the bill increases that will be needed to support better outcomes.

“They also increase pressure on the UK and Welsh governments and Ofwat … to change established regulatory approaches and to set increasingly demanding performance targets.”

Oxera’s Hope backs this up. “If we look at the next five years, the whole industry, particularly the sewerage companies, now have far larger investments to do, because of this public concern about the combined sewer outflows,” he says.

“We’ve gone from a situation where for decades, the investment has been high in the water industry but fairly stable, to one where it’s now going up by multiples. It’s a gear change.”

Ofwat kicks off

This is where the root of the problem seems to lie. Macquarie’s relatively aggressive initial gearing up at Thames Water may not have caused such hardship if it hadn’t collided with Ofwat’s change of approach.

“Borrowing costs increases were the proximate cause that tipped Thames Water over more recently. But the fundamental change was in the regulatory environment, from a framework that balanced the interests of investors and customers to one that was tilted towards getting bills down,” says one long-term investor in the industry.

The public vent frustration at spills, leaks and pollution. Bloomberg

“You can understand that – household budgets were squeezed, there was a political pressure to push the cost of essential services down. But no one foresaw this regulatory change, which happened over the decade from 2009 to 2019.”

The industry’s perspective is that if the regulator does not allow bills to increase substantially, they cannot make the investment in infrastructure upgrades that public and government are demanding. They simply won’t be able to get investors to fund it.

“Ofwat has an unrealistically low idea of a good return on funds employed. Setting that at 4.5 per cent is not investible,” says an executive at one of the water companies.

Earwaker agrees: “There are two conclusions that one might draw at this point,” he wrote. “One might be that water companies just haven’t been up to the task recently and deserve at least some of the criticism they have been receiving. But an alternative view might be that, with the benefit of hindsight, companies were set an impossible challenge five years ago and are now paying the price for regulatory miscalculation.”

The companies have lodged their bids with Ofwat already, and will be looking for some pretty hefty bill increases. Consumer Council for Water chief executive Mike Keil told the BBC that the public would struggle with this. “People do want to see improvements, they do understand that takes investment. But I think the scale of [bill increases] being proposed here is going to come as a real shock.”

Ofwat doesn’t have it easy. If the regulator’s July 11 decision allows the bills to go up too much, it will trigger a political storm. If it doesn’t, it could send more of the water companies to the edge of the financial precipice, and even beyond.

A waste water outflow pipe at low tide on the English south coast. Bloomberg

“Everyone is holding their breath. An aggressive bid from the regulator in the draft that comes out in July would send panic into the market,” says one industry insider.

It is already tough to raise money, he says. “Investors wonder if they can really trust the water regulator, and the politics. Will they ever get a return? You have to raise at a discount to the share price or asset base – that is dilutive and value-destructive.”

Ofwat’s July release is just a draft, with a final determination in December. If the companies challenge that, it could take the Competition and Markets Authority until September next year to resolve the spat.

“Companies would continue to operate but would be in a bit of limbo about what their investment and returns would be,” the insider says.

The industry is vaguely hopeful. One investor says he “can’t see any way forward other than the regulator readjusting the balance a bit more towards investment and financial returns”.

Moody’s and Barclays have expressed similar optimism, but with the caveat that the sector’s politics can be unpredictable.

Either way, Macquarie will still be right in the thick of it. Its utility Southern Water will need to tap the debt markets again in the coming year, and it will need Ofwat to help restore investor confidence.

Southern Water is also not planning to pay a dividend until performance picks up, even though investors in Macquarie Super Core Infrastructure Fund rely on dividend yield as well as capital growth.

Macquarie Asset Management’s head of utilities in Europe, Will Price, says the challenge at Southern, as at all water companies, is to get the Victorian-era combined stormwater and sewerage systems up to scratch, particularly as they come under greater strain from population growth and climate change.

“Another step-change in investment will be needed to deliver new water supplies and leakage reduction alongside a redesign of the waste-water network,” he tells the Financial Review.

“Moving Southern Water from the bottom quarter of the industry league table will take time, but we are focused on providing the financing and skills that are needed to accelerate its transformation.”

Macquarie’s approach to Southern looks and feels very different to the Thames Water story. And the company is certainly keen to make sure of that.

Still, after getting scalded in the British media, it was a bold move on Macquarie’s part to go back into the country’s water sector.

Perhaps the fund managers involved are keeping the words of Greek philosopher Heraclitus pinned to their corkboards: “No man ever steps in the same river twice. For it is not the same river, and he is not the same man.”